The Case for CAC-Based Reforms: or How I Learned to Stop Worrying and Love SDRM Even Though I Think It Should Never Be Implemented

By Gregory Makoff, Author of the Fool Me Twice Substack newsletter and Default: The Landmark Court Battle over Argentina’s $100 Billion Debt Restructuring

Over the last five years I have been repeatedly surprised by the obsession among civil society activists and academics with the IMF’s Sovereign Debt Restructuring Mechanism (SDRM) proposal of 2001. Market observers quickly labeled it a “nuclear bomb solution” and the IMF gave up working on it in 2003 in favor of using Collective Action Clauses (CACs). Yet the idea still resonates twenty-five years later. This baffles me because my job for over twenty years was to help companies and countries restructure their debt. I used to run exchange offers and bondholder votes using CAC features in sovereign and corporate debt. In my experience, they are simple and they work, and we don’t need a complicated, Chapter 11-like SDRM for sovereign debt.

I was an immediate fan of CACs when first used in U.S. sovereign bonds in 2003 and of the more powerful “enhanced CACs” when they were announced by ICMA in August 2014. I liked them because they provided for the aggregated voting of creditors across different series of bonds. I used to manage transactions that involved many separate votes, and they were always risky, logistical nightmares. This topic is visceral to me: I was the guy who got yelled at and had my job threatened if a single vote didn’t pass in a ten series bond restructuring. CACs’ one big vote feature makes a huge difference. In fact, I was so sure that these clauses would make a big difference in the world of sovereign debt restructuring that I spent seven years from 2017 to 2024 writing a book to explain the relationship between the messy Argentina bond litigation after 2005 and the adoption of enhanced CACs in 2014.

Thus I have been gobsmacked over the last few years by the actions of a group of SDRM-inspired academics and activists who have been aggressively promoting an SDRM-like solution in New York State that could override CACs. Why do we need to go back to thinking about this alternative idea when a twenty-five-year effort to put powerful CACs into bonds essentially solved the holdout creditor problem?

I’ll be specific about one of three proposals made in New York over the last few years. This proposal was called a “model law” because it purported to provide a template that could be adopted by other jurisdictions to establish a quasi-SDRM system around the world. The most abhorrent feature of the law is that it would allow the governor to appoint a monitor to oversee sovereign debt restructurings. This was deeply problematic because, in my experience, countries and the IMF already know how to handle debt restructurings and don’t need to hand power over to some new third party. Furthermore, why ask the governor, who is an expert on state-level issues, to appoint an important party to an international negotiation? So, I spoke up in writing against the model law, as did lawyers in New York and London.

Bondholders hated the model law proposal and not only made threatening phone calls to lawmakers but laid the legal groundwork to move the sovereign debt market to Texas in the future if needed. Thankfully, the bigwigs in Albany wisely refused to move on the model law bill, and it is dead as a doornail. Lawmakers in New York listened to bondholders and care what they think! Unfortunately, as a residual hedge against possible future changes to New York law, creditor activists are pushing the idea of adding flip clauses to sovereign bonds, a provision that would give a majority of creditors the right to change a bond’s jurisdiction from New York to another state or country in the future. These bond clauses will, no doubt, lead to disruptive litigation. We have the model law proponents to thank.

This has been a deeply frustrating episode to me, not just as a commentator, but as an active supporter of a narrowly-targeted, pro-market, anti-vulture alternative. But, the long and painful debates over the New York laws got me thinking: Why do so many smart, rational academics and activists—people I count as friends—still find SDRM so attractive while everyone I know from the market, the official community, and governments see it as a clunky, outdated idea? Why does this idea have such staying power?

So I thought, why not put everything on paper to help sort out the differences between my friends who love the idea and those who hate it? Why not write a paper about the great 2001–2003 global financial architecture debate and the subsequent adoption and enhancement of CACs so that people can see the entire story in one place?

The project turned out to be more interesting and fruitful than I anticipated. During two years of research, I not only discovered why SDRM has such staying power, but I also developed a more compelling argument for CACs. Additionally, I came up with a new reform idea inspired by the CAC-SDRM debate. The paper is linked here.

The Powerful Appeal of SDRM and the Underselling of CACs

I have two hypotheses for why SDRM still has so many fans. First, SDRM is widely loved because it presents itself as a powerful, comprehensive, and necessary solution to the very complex problem of sovereign debt restructuring. Second, CACs are underappreciated because the US Treasury failed to clearly explain how they could serve as the basis of a comprehensive sovereign debt restructuring system.

SDRM naturally appeals to intellectuals because it was a big, bold proposal to solve a pressing global problem. Anne Krueger’s announcement of the idea on November 26, 2001, was breathtaking in scope and power. She decried that private creditors had become increasingly “numerous, anonymous, and difficult to coordinate.” She said there was a “gaping hole” in the architecture to resolve sovereign debt distress. And she said there were “vulture funds” including Elliott Associates already preying on poor countries, including Peru. And she was right, as Argentina’s December 2001 default soon proved.

The problem with SDRM today is that Anne Krueger’s big bold idea did not make it through the approval process intact. Instead, it was watered down between 2001 and 2003 as it moved from concept towards execution. Anne Krueger’s proposal had the IMF setting up the scheme and running the show, but by 2003 the IMF no longer had a role in approving litigation stays or plans of adjustment. The weakest feature of the revised SDRM, in my opinion, was that to obtain a stay of litigation (i.e. to enter the SDRM), a country would have to obtain the support of a majority of creditors. We know from the history of US municipal bankruptcy law that this is an awful idea: Before 1976, municipal bond restructuring in the United States required a 51% creditor vote, but this gating provision was removed in 1975 when it became obvious that bondholders would block New York City’s critical bankruptcy filing. A workable insolvency system needs an automatic stay, not one that is creditor gated.

The sad truth is that SDRM flip-flopped from too strong for the market to too weak to get the job done. The idea was brilliant in theory, but unworkable in practice. Too few people understand this today because they have only read Anne Krueger’s visionary speech and perhaps the IMF’s initial aspirational proposals and not the painfully complicated revisions that followed—Sean Hagan’s “Designing a Legal Framework to Restructure Sovereign Debt” is an excellent source for details.

In addition to its infeasibility, the revised SDRM had an additional problem: The scope of debt it covered was substantially narrowed between 2001 and 2003. Initially, SDRM aspired to cover a country’s commercial, bilateral, and local debt. But by 2003, it had been scaled back to cover only commercial debt. The problem was that the IMF staff couldn’t persuade countries to cede control of their sovereign borrowing and lending to the SDRM authority—sovereignty got in the way.

The result of the IMF’s backtracking is that neither SDRM nor CACs are as comprehensive as Chapter 11; both cover one category of sovereign debt—commercial debt. As a consequence, the choice between CACs or SDRM was reduced to which would do a better job of restructuring commercial debt. At the time, the IMF argued that SDRM was better because CACs would never include more powerful, aggregated voting that SDRM would include. Even the US Treasury had doubts, which is why it proposed less powerful, single-series voting CACs to the market. Time has proven both wrong as the market accepted super powerful CACs with aggregated voting in 2014. To be sure, both the IMF and US Treasury were right to be skeptical because it took the mindbogglingly disruptive Argentina bond litigation to convince the market to make the jump.

The selection of the optimal approach today is further narrowed because CACs and SDRM both provide for aggregated voting. The decision on approach therefore reduces to the question of cost and ease of operation. CACs, I believe, win this battle easily because judicial type procedures operate slowly and force huge legal expenses onto the debtor. This is well documented for the field of corporate insolvency and by the $2.1 billion-dollar, six-year process to restructure the debt of the Commonwealth of Puerto Rico in a federal court.

The powerful strengthening of CACs and their widespread adoption proves that policymakers made the right decision to go with CACs in 2003. And there is absolutely no reason to switch to an SDRM approach now. Yet activists and academics persist in promoting the idea, including at the United Nations.

But love of SDRM is only half the problem. Distrust of CACs is the flipside. As an automatic believer in CACs (from my corporate debt experience) this lack of trust in a well-known, widely-used legal mechanism has long mystified me. But while spending time with the records of the CAC-SDRM debate I discovered that the U.S. Treasury did not do a great job selling CACs as an alternative.

U.S. Undersecretary for International Affairs John B. Taylor made eloquent speeches explaining how CACs would solve the holdout creditor problem in sovereign bonds. He also explained that it was a much more workable solution than SDRM: just drop CACs into bonds—no treaty negotiations and no going to Congress needed. But he and his team failed to explain how the entire debt restructuring process would work using CACs. It looked like part of a solution. And this apparent gap in coverage of the problem left a lot of observers feeling short-changed when the U.S. Treasury pushed SDRM off the agenda.

The contract-based approach, in effect, has a legitimacy problem among academics and activists. SDRM looked like comprehensive system while CACs didn’t. This perception is understandable in light of the particulars of the 2002-2003 debate. But today there is no gap. Policymakers and practitioners have built up a deep understanding of how debt restructuring works with CACs through their use in many transactions since 2003. This makes it possible for me to now explain what Treasury did not adequately explain in 2002–2003: how CACs function as part of a comprehensive sovereign debt restructuring system that effectively addresses all stakeholder groups.

CAC-based restructurings work because countries restructure their bilateral debt, domestic debt, and commercial debt in parallel. They obtain comprehensive Chapter 11-like results because countries work with the IMF to assure that the totality of debt relief granted from their various stakeholders is sufficient to restore debt sustainability. The legal/commercial mechanism to assure a coherent outcome is cross-conditionality. Each stakeholder group commits to providing debt conditional on the other groups doing their part. The IMF provides some glue, too, because it’s lending is generally conditioned on all the different stakeholder groups completing the needed transactions. It is a comprehensive system that works.

In this scheme, Collective Action Clauses are central. They do the heavy lifting by solving the problem of coordinating the country’s many bondholders, who cannot be effectively coordinated though ad-hoc conditionality. In contrast, bilateral lenders, local lenders, and bank lenders are managed separately through cross-conditional settlement. I am not saying it’s easy! I am just saying that there is no unsolvable legal problem here that requires an international treaty and a judge in a wig to resolve.

Theoretically, we should think of sovereign debt restructuring not as a collective action problem but a collection of dissimilar collective action problems. There is the collective action problem of getting bondholders to agree on terms, which is solved by CACs. But then there is the collective action problem of getting bilateral creditors to agree on terms, which is political in character. This is a useful distinction. For example, the identification of the bilateral creditor problem as a political problem explains the success of the recently established Global Sovereign Debt Roundtable (GSDR) in easing tensions between bilateral lenders over the negotiation of debt restructuring deals since 2020. The GSDR was an effective reform because it was a diplomatic approach to solving a diplomatic problem.

From CACs to Stays

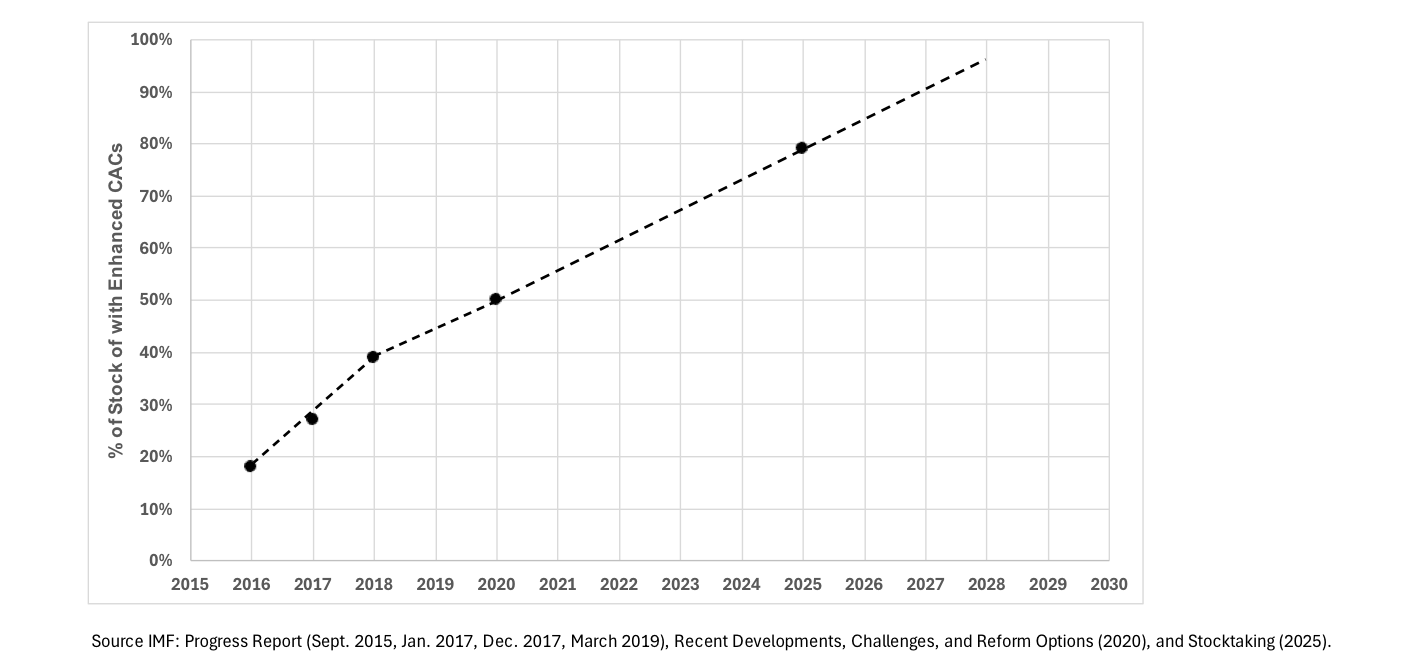

The case for CACs is stronger than ever in light of the IMF’s 2025 stocktaking report that documents the near-universal adoption of enhanced CACs since 2020—see Figure One for the numbers, which are taken from the IMF’s periodic updates since 2016.

Figure One: Realized and Projected Adoption of Enhanced CAC’s in Sovereign Bonds

Yet I am no SDRM hater. I love Anne Krueger’s great speech of November 2001, and I use it as the opening scene of my book, Default. In the speech she set out a great vision for solving a very real problem of the world. And it led to meaningful action. Moreover, re-reading the CAC-SDRM debate material gave me a new idea.

What sticks out of from the side-by-side comparison of CACs and SDRM in my paper is the lack of a litigation stay under the contract-based approach. So, I thought, why don’t we add a stay? After all, an orderly insolvency system needs two essential working parts: an aggregation mechanism and a stay of litigation.

Helpfully, the power to stay sovereign debt litigation already exists under U.S. law. Since the early 1990s U.S. federal judges have regularly stayed litigation and/or enforcement to facilitate sovereign debt restructurings. Stays (or analogous orders) were granted to protect against holdout litigation against Peru in the 1990s. Stays were granted to the benefit of Argentina in the 2000s. And, more recently, the judge in the litigation against Sri Lanka did the same after receiving an amicus brief from the U.S. government.

The problem, however, is that these stays are ad-hoc in nature and, generally, of a limited duration. The Foreign Sovereign Immunities Act says that judges may delay enforcement for a reasonable period of time. The law does not contemplate open-ended stays covering the one-to-two-year period needed for a country to restructure its debt.

The Argentina bond restructuring of 2005 is instructive of the weakness of the stay protection offered under current law. Judge Griesa granted a succession of short duration stays of enforcement in 2003. But he did not extend the stays past the end of 2003 because he was not comfortable that the law allowed him to do so. The result was that when Argentina sought to close its debt restructuring in 2005, creditors tried to interfere. As discussed in Default, Elliott Associates and other plaintiffs made a motion to attach some of the bonds to be cancelled as part of the operation, which would have taken away its debt reduction benefits. The plaintiffs were unsuccessful, but the litigation over the attachment delayed the settlement of the transaction for about three months. Judge Griesa should have simply been able to stay all attachment efforts through the duration of Argentina’s debt restructuring process. Thus, the Foreign Sovereign Immunities Act should be amended to give federal judges the explicit power to grant stays for the duration of sovereign debt negotiations, subject, let’s say, to continuing good faith negotiations between the parties.

A Guideline for Future Reform Efforts

The near universal adoption of CACs and their successful use suggest an important guideline. I propose that the goal of new sovereign debt reform initiatives should be to make CAC-facilitated restructurings work better.

The stay proposal above fits this definition: Its function would be to let countries and their creditors settle insolvencies via CACs without disruption from court actions. This proposed reform is statutory, but all sorts of potential reforms fall under the CAC-supporting rubric, including further evolution of debt contracts and changes in IMF and World Bank policy.

Remaining problems to solve include: 1) the universe of sovereign bonds without enhanced CACs; 2) countries issuing new loans without aggregated voting; and 3) the use of State-Owned Entities to hide debt and make it hard to restructure. These are not unsolvable problems in the CAC approach. Countries borrowing opaquely, for example, could be controlled by debtor education, new reporting provisions in sovereign bonds, and the IMF and World Bank conditioning loans on full and accurate disclosure of all debt. The problem of countries issuing sovereign loans without CACs could be managed by putting a hard cap on the amount of non-enhanced CAC commercial borrowing in bond covenants to limit their use.

The greatest benefit of the CAC approach is that it is flexible. All that is needed to make a change is for the G-20 and bond market leaders to come to agreement on terms. Changing contracts, IMF and World Bank policy, and statutes should not take long if backed by a global consensus. Therefore, the focus of reformers going forward should be on developing CAC-supportive ideas and presenting them to this broad group of stakeholders. So, let’s give SDRM a respectful rest and travel together in this direction.

“Countries borrowing opaquely, for example, could be controlled by debtor education, new reporting provisions in sovereign bonds, and the IMF and World Bank conditioning loans on full and accurate disclosure of all debt. “ LOL. Take Senegal, where the Bank and the Fund allowed Senegal to borrow off-budget for corrupt projects and are refusing to sanction any of their staff for failing to see what the borrower was doing.

What do you think about the resolution of this appeal https://www.batimes.com.ar/news/economy/us-court-overturns-us16-billion-judgment-against-argentina-over-ypf-nationalisation.phtml